Patelco Home Equity Loan Interest Rates

Securing a home equity loan can be a powerful financial tool, allowing you to leverage your home’s equity for various needs, from home improvements to debt consolidation. Understanding the interest rates associated with these loans is crucial for making informed financial decisions. This section will delve into Patelco’s home equity loan interest rates, comparing them to competitors and examining the factors that influence their determination.

Patelco Home Equity Loan Interest Rates Compared to Competitors

Understanding how Patelco’s rates stack up against the competition is vital. The following table compares Patelco to three major competitors, offering a snapshot of interest rate ranges, loan terms, and associated fees. Keep in mind that these rates are subject to change and are based on current market conditions. Always verify the most up-to-date information directly with the lender.

| Lender | Interest Rate Range (APR) | Loan Terms (Years) | Fees |

|---|---|---|---|

| Patelco Credit Union | 6.5% – 12% (Example Range – Actual rates vary based on creditworthiness and loan amount) | 5-15 | Loan origination fee (variable), appraisal fee (if required) |

| Competitor A (Example: Bank of America) | 7% – 13% (Example Range – Actual rates vary) | 5-15 | Loan origination fee, appraisal fee, potential early payoff penalties |

| Competitor B (Example: Wells Fargo) | 7.5% – 14% (Example Range – Actual rates vary) | 10-20 | Loan origination fee, appraisal fee, potential early payoff penalties |

| Competitor C (Example: Chase) | 8% – 15% (Example Range – Actual rates vary) | 5-15 | Loan origination fee, appraisal fee, potential early payoff penalties |

Factors Influencing Patelco’s Home Equity Loan Interest Rates

Several factors contribute to the specific interest rate Patelco offers on its home equity loans. These factors reflect the lender’s assessment of risk and the prevailing market conditions. A higher perceived risk translates to a higher interest rate.

- Credit Score: A higher credit score indicates lower risk, resulting in a potentially lower interest rate. A borrower with a FICO score above 750 might qualify for a significantly lower rate than someone with a score below 650.

- Loan-to-Value Ratio (LTV): The LTV is the ratio of the loan amount to the value of your home. A lower LTV (meaning you’re borrowing less relative to your home’s worth) generally leads to a lower interest rate because it represents less risk to the lender.

- Market Interest Rates: Prevailing interest rates in the broader financial market significantly impact the rates offered by lenders. When overall interest rates rise, so do home equity loan rates, and vice versa.

- Debt-to-Income Ratio (DTI): Your DTI, which compares your monthly debt payments to your gross monthly income, is a key indicator of your ability to repay the loan. A lower DTI generally results in a more favorable interest rate.

- Loan Amount and Term: Larger loan amounts and longer loan terms may carry slightly higher interest rates due to increased risk for the lender.

Patelco’s Interest Rates Compared to National Averages

Determining the precise national average for home equity loan interest rates requires referencing multiple sources and averaging them across various lenders. However, we can use publicly available data from reputable financial websites to gain a general idea. For example, if the national average for a home equity loan with similar terms to Patelco’s offering is around 8%, and Patelco’s range is 6.5% to 12%, this indicates that Patelco’s rates can be competitive, depending on the borrower’s specific circumstances. It’s crucial to compare offers from multiple lenders to ensure you’re securing the best possible rate.

Patelco Home Equity Loan Eligibility Requirements

Securing a home equity loan can be a powerful financial tool, allowing you to leverage your home’s equity for various needs. However, understanding the eligibility requirements is crucial before you begin the application process. Patelco, like other lenders, has specific criteria to assess your application and determine your eligibility for a home equity loan. This section will clearly Artikel these requirements to help you determine your readiness.

Eligibility for a Patelco home equity loan hinges on several key factors. These factors are designed to ensure both your financial well-being and the lender’s ability to manage risk effectively. A thorough understanding of these criteria will streamline your application process and increase your chances of approval.

Minimum Credit Score, Debt-to-Income Ratio, and Loan-to-Value Ratio Requirements

Meeting certain financial benchmarks is fundamental to securing a home equity loan. Lenders use these metrics to gauge your creditworthiness and ability to repay the loan. Failure to meet these minimum requirements often leads to loan application rejection. Let’s break down the key metrics.

- Minimum Credit Score: While Patelco doesn’t publicly state a specific minimum credit score, expect a score significantly above 620 for favorable consideration. Higher credit scores typically translate to better interest rates and loan terms. A score below 620 significantly reduces your chances of approval.

- Debt-to-Income Ratio (DTI): Your DTI is the percentage of your gross monthly income that goes towards debt payments. Patelco likely prefers a lower DTI, ideally below 43%, although this can vary depending on other factors in your application. A lower DTI demonstrates your capacity to manage existing debt and handle additional loan payments. For example, a borrower with a gross monthly income of $10,000 and total monthly debt payments of $3,000 would have a DTI of 30% (3000/10000 * 100).

- Loan-to-Value Ratio (LTV): The LTV is the ratio of the loan amount to the value of your home. Lenders typically prefer a lower LTV, as it indicates less risk. Patelco’s specific LTV requirements may vary, but generally, a lower LTV increases your chances of approval and may result in better loan terms. For instance, an LTV of 80% means you’re borrowing 80% of your home’s value.

Documentation Needed for a Patelco Home Equity Loan Application

Preparing the necessary documentation beforehand significantly speeds up the application process. Having all the required documents ready ensures a smoother and more efficient experience. The following list represents the typical documentation requested by lenders for home equity loan applications.

- Proof of Income: This typically includes pay stubs, W-2 forms, tax returns, or bank statements showing consistent income.

- Proof of Homeownership: Provide your mortgage statement or deed to demonstrate ownership of the property.

- Home Appraisal: Patelco may require a professional appraisal to determine the current market value of your home, especially if you haven’t recently had one done.

- Credit Report: A copy of your credit report will be needed to assess your creditworthiness.

- Bank Statements: Several months of bank statements to verify your financial history and stability.

Patelco Home Equity Loan Pre-qualification Process

Pre-qualification is a crucial step that allows you to understand your potential eligibility without a formal application. This process provides a preliminary assessment of your chances of approval and helps you estimate the loan amount you might qualify for. It allows you to shop around for the best rates and terms before committing to a full application.

- Initial Inquiry: Contact Patelco directly through their website or a branch. Provide basic information such as your income, credit score (if known), and the estimated value of your home.

- Credit Check (Soft Pull): Patelco will likely perform a soft credit check, which doesn’t impact your credit score. This allows them to get a preliminary understanding of your credit history.

- Preliminary Approval: Based on the information provided, Patelco will provide a preliminary indication of your eligibility and a potential loan amount. This is not a formal loan approval, but it gives you a good idea of your chances.

- Next Steps: If pre-qualified, you can then proceed with a formal application, providing the full documentation mentioned previously.

Patelco Home Equity Loan Application Process

Applying for a Patelco home equity loan might seem daunting, but breaking it down into manageable steps simplifies the process. Understanding the different loan types and the typical processing time will help you manage your expectations and prepare effectively. Remember, a well-prepared application can significantly speed up the approval process.

Patelco offers various home equity loan options to suit diverse financial needs. Understanding these options is crucial for selecting the best fit for your specific circumstances. The application process itself is streamlined to ensure a smooth and efficient experience.

Patelco Home Equity Loan Options

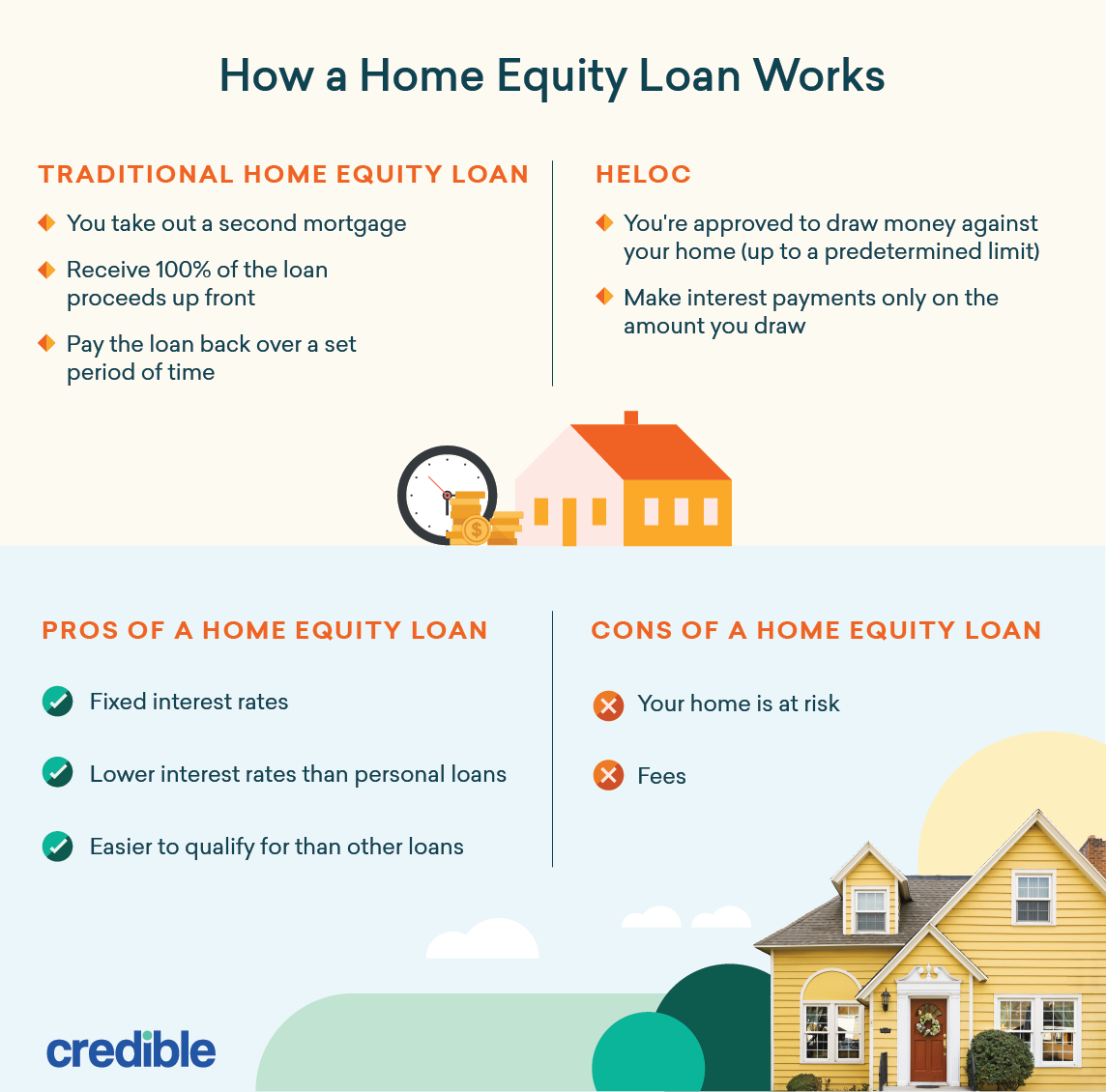

Patelco likely offers two primary types of home equity loans: Home Equity Lines of Credit (HELOCs) and fixed-rate home equity loans. A HELOC functions like a credit card, allowing you to borrow against your home’s equity up to a certain limit, with interest charged only on the amount borrowed. A fixed-rate home equity loan, conversely, provides a lump-sum disbursement with a fixed interest rate and repayment schedule over a set term. Choosing between these depends on your financial goals and risk tolerance. A HELOC offers flexibility, while a fixed-rate loan provides predictable monthly payments.

Step-by-Step Application Process

The application process typically involves several key steps. While the exact steps may vary slightly, this Artikel provides a general overview. It’s always best to confirm the current process directly with Patelco.

- Pre-qualification: Before formally applying, consider pre-qualifying. This involves providing basic financial information to receive an estimate of how much you might borrow. This helps you gauge your borrowing power without impacting your credit score.

- Gather Required Documents: Prepare all necessary documentation. This usually includes proof of income, employment history, tax returns, and details about your property. Having these readily available streamlines the process significantly.

- Complete the Application: Fill out the formal loan application accurately and completely. Any inaccuracies or omissions can delay the process. Double-check all information before submitting.

- Credit Check and Appraisal: Patelco will conduct a credit check and likely order an appraisal of your home to determine its current market value and assess your equity. This is a standard procedure for all home equity loans.

- Loan Approval or Denial: Based on the review of your application, documents, credit score, and appraisal, Patelco will notify you of their decision. If approved, you’ll receive loan terms and conditions.

- Loan Closing: Once you accept the loan terms, the closing process begins. This involves signing the final loan documents and receiving the loan proceeds. This step typically involves legal and administrative procedures.

Typical Processing Time, Patelco home equity loan

The time it takes to process a Patelco home equity loan application can vary depending on several factors, including the complexity of your application, the availability of required documentation, and the appraisal process. While Patelco might provide an estimated timeframe, it’s wise to anticipate a processing period ranging from several weeks to a couple of months. A complete and accurate application will help expedite the process. Unexpected delays might arise due to unforeseen circumstances such as appraisal backlogs or required clarifications.

Patelco Home Equity Loan Repayment Options

Understanding your repayment options is crucial for successfully managing your Patelco home equity loan. Choosing the right repayment plan can significantly impact your monthly budget and overall loan cost. Let’s explore the various repayment structures available and how to choose the one that best suits your financial situation.

Patelco Home Equity Loan Repayment Options Summary

Patelco offers flexible repayment options tailored to individual needs. The specific options available to you may depend on your loan terms and agreement. Below is a summary of common repayment structures.

| Repayment Type | Description |

|---|---|

| Fixed-Rate Monthly Payments | This is the most common type. You’ll make equal monthly payments over the loan term, with a consistent principal and interest portion. This provides predictability in your budgeting. |

| Variable-Rate Monthly Payments | Your monthly payment amount can fluctuate based on changes in the index rate used to calculate your interest rate. This can lead to unpredictable payments, potentially increasing or decreasing over time. |

| Accelerated Payment Options | Patelco may offer options to make extra principal payments to reduce your loan term and overall interest paid. This can save you money in the long run. |

| Bi-Weekly Payments | Making half your monthly payment every two weeks can significantly reduce the total interest paid over the life of the loan. This effectively results in an extra monthly payment each year. |

Sample Amortization Schedule

The following is a sample amortization schedule for a $50,000 home equity loan with a 10-year term and a 6% annual interest rate. Remember that this is a simplified example, and your actual schedule may vary slightly depending on your specific loan terms.

| Month | Beginning Balance | Payment | Interest | Principal | Ending Balance |

|---|---|---|---|---|---|

| 1 | $50,000.00 | $597.68 | $250.00 | $347.68 | $49,652.32 |

| 2 | $49,652.32 | $597.68 | $248.26 | $349.42 | $49,302.90 |

| 3 | $49,302.90 | $597.68 | $246.51 | $351.17 | $48,951.73 |

| … | … | … | … | … | … |

| 120 | $0.00 | $597.68 | $0.00 | $597.68 | $0.00 |

*(Note: This is a simplified example and does not include potential fees or taxes. A complete amortization schedule would include all such charges.)*

Consequences of Late or Missed Payments

Late or missed payments on your Patelco home equity loan can have serious financial consequences. These include:

* Late fees: Patelco will likely charge late fees for each missed or late payment. These fees can add up significantly over time.

* Damage to credit score: Late payments are reported to credit bureaus, negatively impacting your credit score. A lower credit score can make it harder to obtain future loans or credit at favorable rates.

* Increased interest rates: Repeated late payments may lead to an increase in your interest rate, increasing the total cost of your loan.

* Loan acceleration: In severe cases of consistent late payments, Patelco may accelerate your loan, requiring you to repay the entire remaining balance immediately. This could lead to foreclosure if you are unable to repay the loan in full.

* Collection actions: If you fail to make payments, Patelco may pursue collection actions, which can include lawsuits and wage garnishment.

Patelco Home Equity Loan Fees and Charges

Understanding the complete cost of a home equity loan is crucial for making an informed financial decision. While the interest rate is a significant factor, various fees and charges can significantly impact the overall expense. Failing to account for these additional costs can lead to unexpected financial burdens. Let’s break down the typical fees associated with a Patelco home equity loan and compare them to a competitor.

Patelco, like most lenders, charges several fees associated with obtaining a home equity loan. These fees can vary depending on the loan amount, your creditworthiness, and the specifics of your loan agreement. It’s always best to obtain a Loan Estimate from Patelco to get a precise breakdown for your situation.

Patelco Home Equity Loan Fee Breakdown

Several fees can be associated with a Patelco home equity loan. Understanding these fees upfront allows for better budgeting and financial planning.

- Appraisal Fee: This fee covers the cost of a professional appraisal to determine the current market value of your home. This is essential for the lender to assess the loan-to-value ratio (LTV).

- Loan Origination Fee: This fee compensates the lender for processing your loan application and setting up the loan. It’s typically a percentage of the loan amount.

- Closing Costs: These encompass various expenses associated with finalizing the loan, including title insurance, recording fees, and other administrative charges. These costs can vary significantly.

- Prepayment Penalty (Potential): While not always present, some home equity loans may include a prepayment penalty if you pay off the loan early. This penalty is designed to compensate the lender for lost interest income.

- Late Payment Fees: If you fail to make your monthly payments on time, Patelco will likely charge a late payment fee. The amount of this fee will be specified in your loan agreement.

Impact of Fees on Overall Loan Cost

These fees, while seemingly small individually, can collectively add a substantial amount to the overall cost of your home equity loan. Let’s illustrate this with an example.

| Fee | Amount |

|---|---|

| Loan Origination Fee (1%) | $2,000 (on a $200,000 loan) |

| Appraisal Fee | $500 |

| Closing Costs | $1,500 |

| Total Fees | $4,000 |

In this example, the total fees amount to $4,000, representing a significant addition to the principal loan amount. This needs to be factored into your total borrowing cost and monthly payment calculations. Remember, this is just an example; your actual fees will vary.

Fee Comparison with a Competitor

Comparing Patelco’s fee structure to a competitor requires knowing the specific fees charged by that competitor. However, we can illustrate a general comparison. Let’s assume a competitor, “Credit Union X,” charges a 0.75% origination fee, a $400 appraisal fee, and $1,200 in closing costs on a similar $200,000 loan.

| Lender | Origination Fee | Appraisal Fee | Closing Costs | Total Fees |

|---|---|---|---|---|

| Patelco | $2,000 (1%) | $500 | $1,500 | $4,000 |

| Credit Union X | $1,500 (0.75%) | $400 | $1,200 | $3,100 |

This comparison demonstrates that while the fees can vary, a thorough comparison of all fees is essential before selecting a lender. Always obtain a Loan Estimate from multiple lenders to make the most informed decision.

Patelco Home Equity Loan Advantages and Disadvantages

Choosing a home equity loan, like any financial decision, requires careful consideration of both its potential benefits and drawbacks. Understanding these aspects is crucial for making an informed choice that aligns with your financial goals and risk tolerance. This section will Artikel the advantages and disadvantages of a Patelco home equity loan, helping you weigh the pros and cons before proceeding.

Advantages of a Patelco Home Equity Loan

A Patelco home equity loan offers several potential advantages, making it an attractive option for some homeowners. These benefits, however, should be carefully weighed against the associated risks.

- Lower Interest Rates: Home equity loans often come with lower interest rates compared to other forms of borrowing, such as personal loans or credit cards. This can result in significant savings on interest payments over the loan term. For example, a homeowner might secure a rate of 5% on a home equity loan versus 10% on a personal loan, resulting in substantial cost savings.

- Large Loan Amounts: Home equity loans allow you to borrow a substantial amount of money, often significantly more than with other loan types. This can be beneficial for large expenses like home renovations, debt consolidation, or significant medical bills. The amount you can borrow is typically based on your home’s equity.

- Fixed Interest Rates: Many home equity loans offer fixed interest rates, providing predictability and stability in your monthly payments. This eliminates the risk of fluctuating interest rates that can impact your budget unpredictably, as seen with adjustable-rate mortgages.

- Tax Deductibility (Potentially): Interest paid on a home equity loan may be tax-deductible, depending on your circumstances and how the loan proceeds are used. Consult a tax professional to determine your eligibility for this deduction. This deduction can significantly reduce your overall tax burden.

Disadvantages of a Patelco Home Equity Loan

While home equity loans offer certain benefits, it’s crucial to acknowledge the potential drawbacks. Failing to understand these risks can lead to financial difficulties.

- Risk of Foreclosure: The biggest risk associated with a home equity loan is the potential loss of your home if you fail to make your payments. This is because your home serves as collateral for the loan. Defaulting on the loan can lead to foreclosure proceedings.

- High Debt-to-Income Ratio: Taking out a home equity loan can increase your debt-to-income ratio, potentially impacting your credit score and making it harder to obtain future loans. A high debt-to-income ratio signals higher financial risk to lenders.

- Limited Access to Equity: Once you’ve taken out a home equity loan, you have less access to your home’s equity for future borrowing needs. This can restrict your financial flexibility in the future.

- Fees and Charges: Home equity loans often involve various fees and charges, including origination fees, appraisal fees, and closing costs. These fees can add to the overall cost of the loan and should be factored into your budget.

Potential Risks of a Patelco Home Equity Loan

The risks involved in a Patelco home equity loan primarily stem from the use of your home as collateral. Understanding these risks is critical for responsible borrowing. Failure to make timely payments could result in serious financial consequences.

The most significant risk is foreclosure. If you cannot make your monthly payments, Patelco could foreclose on your home, leading to its sale and potentially a significant financial loss for you. This scenario can be particularly devastating if the value of your home has decreased since you took out the loan. Furthermore, a negative impact on your credit score due to defaulting on the loan can make it difficult to secure future credit, impacting your ability to buy a car, purchase a new home, or even obtain a credit card.

Another critical risk involves overextending your finances. Borrowing more than you can comfortably repay can lead to a cycle of debt that is difficult to break. It’s essential to carefully assess your income, expenses, and debt levels before applying for a home equity loan. A realistic budget is paramount to avoid financial strain and potential default.

Patelco Home Equity Loan Customer Service and Support

Securing a home equity loan is a significant financial decision, and having access to reliable and responsive customer service is crucial throughout the process. Patelco Credit Union understands this, offering various support channels to assist borrowers with their home equity loan needs. Understanding these options and the typical customer experiences is key to making an informed choice.

Patelco provides multiple avenues for customers to receive assistance with their home equity loans. These channels allow for diverse communication preferences and varying levels of urgency. The availability and responsiveness of these channels directly impact customer satisfaction and overall loan experience.

Contact Channels for Patelco Home Equity Loan Support

Patelco offers several ways for borrowers to connect with their customer service team. These options provide flexibility and convenience, catering to individual preferences.

- Phone Support: Patelco provides a dedicated phone number for home equity loan inquiries. Representatives are available during specified business hours to answer questions, address concerns, and provide assistance with account management. The phone number is prominently displayed on their website and loan documents.

- Email Support: For non-urgent inquiries or to provide documentation, borrowers can utilize Patelco’s email support system. While response times may vary, email provides a written record of communication for future reference.

- Online Chat: Many credit unions now offer online chat support, and Patelco may provide this option on their website. This allows for real-time communication with a customer service representative for immediate answers to simple questions.

- In-Person Support: Patelco has physical branches, and visiting a branch allows for face-to-face interaction with a loan specialist. This is beneficial for complex issues or situations requiring in-depth discussion.

Customer Feedback on Patelco Home Equity Loan Customer Service

Understanding the experiences of previous Patelco home equity loan customers provides valuable insight into the quality of their support. Analyzing customer reviews and feedback helps gauge the effectiveness and responsiveness of the support channels.

- Positive Feedback: Many customers report positive experiences with Patelco’s customer service, citing helpful and knowledgeable representatives who efficiently address their inquiries. Some praise the ease of contacting customer service through various channels.

- Negative Feedback: Some customers have reported longer-than-desired wait times, particularly during peak hours. Occasionally, inconsistencies in response times across different communication channels have been noted. A small percentage of customers report difficulty reaching a live representative or experiencing challenges navigating the online support resources.

- Overall Sentiment: While some negative experiences exist, the overall sentiment regarding Patelco’s home equity loan customer service tends to be positive, reflecting a generally helpful and responsive support team.

Online Resources for Patelco Home Equity Loan Borrowers

Patelco’s website serves as a valuable resource for borrowers seeking information and support related to their home equity loans. The website provides access to essential documents, FAQs, and other helpful tools.

- Frequently Asked Questions (FAQs): The website likely features a comprehensive FAQ section addressing common questions regarding loan applications, interest rates, repayment options, and other pertinent information. This self-service resource can quickly resolve many common inquiries.

- Account Access and Management: Secure online account access allows borrowers to monitor their loan balance, view payment history, and manage their account settings. This online portal provides convenient access to key information 24/7.

- Loan Documents and Forms: The website provides access to downloadable loan documents, applications, and forms, streamlining the process of obtaining necessary information and completing required paperwork.